Table of Contents

- What Is DTI in Finance?

- How Is DTI Calculated?

- What Is a DTI Code?

- Why DTI Codes Matter?

- Where Are DTI Codes Used?

- Why is DTI Important?

- Types of DTI: Front-End vs. Back-End

- What’s a Good DTI Ratio?

- How to Improve Your DTI Code?

- DTI Code vs. Credit Score

- DTI and Mortgages

- Common Myths About DTI Codes

- Real-Life Example

- Final Thoughts

In finance, it’s easy to feel overwhelmed by codes, numbers, and terms that sound overly technical. One such term is DTI, short for Debt-to-Income ratio. While many people are familiar with DTI, fewer understand what a DTI code is and its significance. Whether you’re applying for a mortgage, car loan, or managing your credit profile, understanding your DTI code can give you a serious edge.

What Is DTI in Finance?

DTI (Debt-to-Income ratio) is a simple formula used by banks and lenders to understand how much of your income goes toward debt payments. It helps them determine if you can take on new debt responsibly.

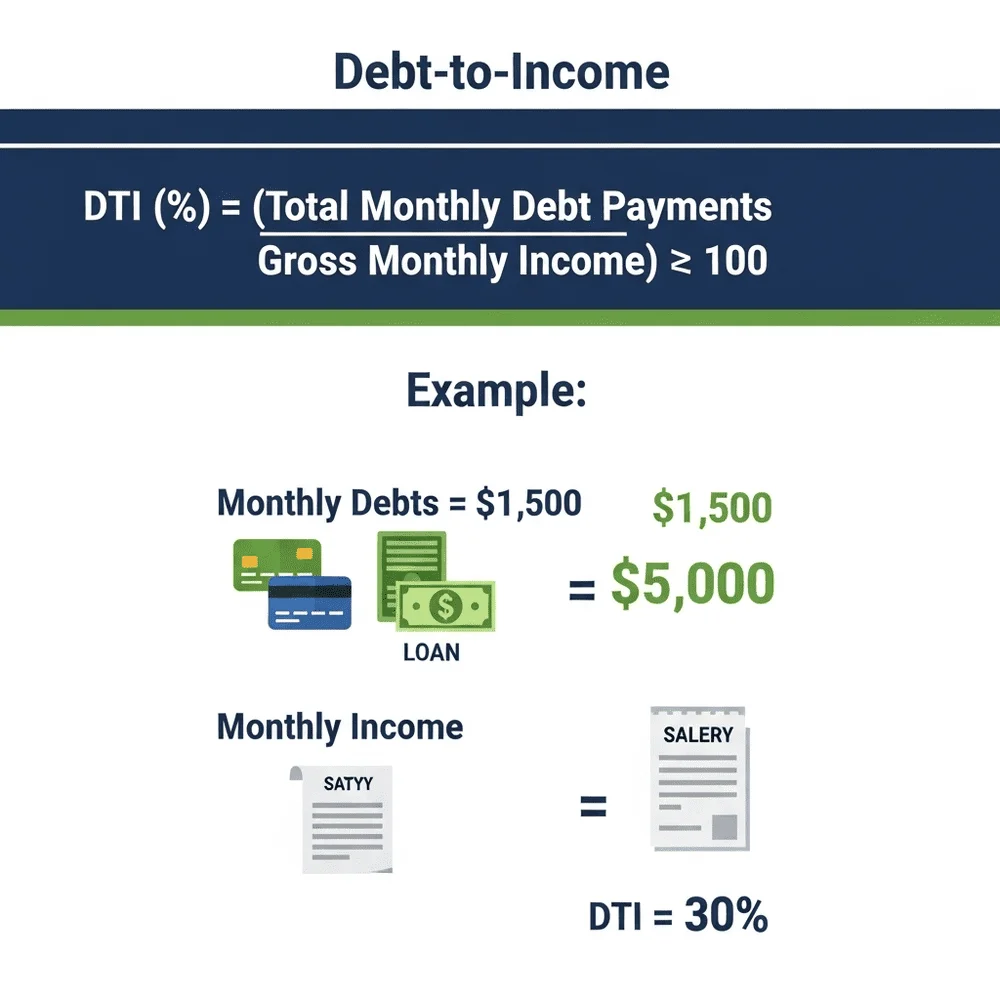

How Is DTI Calculated?

Here’s the basic formula:

Debt-to-Income Ratio (%) = (Total Monthly Debt Obligations ÷ Gross Monthly Earnings) × 100

Example:

- Monthly debts: $1,500

- Monthly income: $5,000

- DTI = (1500 ÷ 5000) × 100 = 30%

This percentage shows how much of your earnings are already committed to debt, and the lower it is, the better.

What Is a DTI Code?

While DTI is a percentage, a DTI code is a categorical label or numerical identifier used by financial systems to quickly assess your risk profile. These codes help banks and lenders process applications faster without manually analyzing every detail.

Think of DTI codes as shortcuts that categorize borrowers:

| DTI Code | DTI Range | Risk Level |

| Code 1 | Under 20% | Excellent (Low Risk) |

| Code 2 | 21% – 35% | Good (Manageable) |

| Code 3 | 36% – 45% | Fair (Watch List) |

| Code 4 | Over 45% | Risky (High Risk) |

Different institutions may use slightly different ranges or labels, but the purpose remains the same: to assess loan eligibility efficiently.

Why DTI Codes Matter?

Your DTI code is not just a number behind the scenes; it actively influences how lenders treat your application. Here’s how:

- Loan Approval: A lower code increases your chances of approval.

- Interest Rates: A high DTI code may result in elevated interest rates, as lenders view such borrowers as higher risk.

- Loan Amounts: Lenders may reduce the loan size offered to high-code applicants.

- Credit Health Indicator: It serves as a rapid assessment of your overall financial stability.

Where Are DTI Codes Used?

DTI codes appear in many places across the financial ecosystem:

- Mortgage loan applications

- Personal loan systems

- Credit risk reports

- Internal bank underwriting tools

- Government-backed loan programs (FHA, VA)

These codes automate decision-making, helping financial institutions process thousands of applications efficiently.

Why is DTI Important?

Financial institutions rely on your DTI code to evaluate your ability to manage additional debt obligations. If your DTI is too high, they may think you are financially stressed or may default on payments. A low DTI shows that you manage your finances well and have room for new loans.

Lenders use your DTI to:

- Approve or deny a loan or credit application

- Decide on your interest rate

- Set your credit limit

- Determine your loan amount

- Assess your repayment ability

This ratio gives lenders a quick look at your financial habits and risk level.

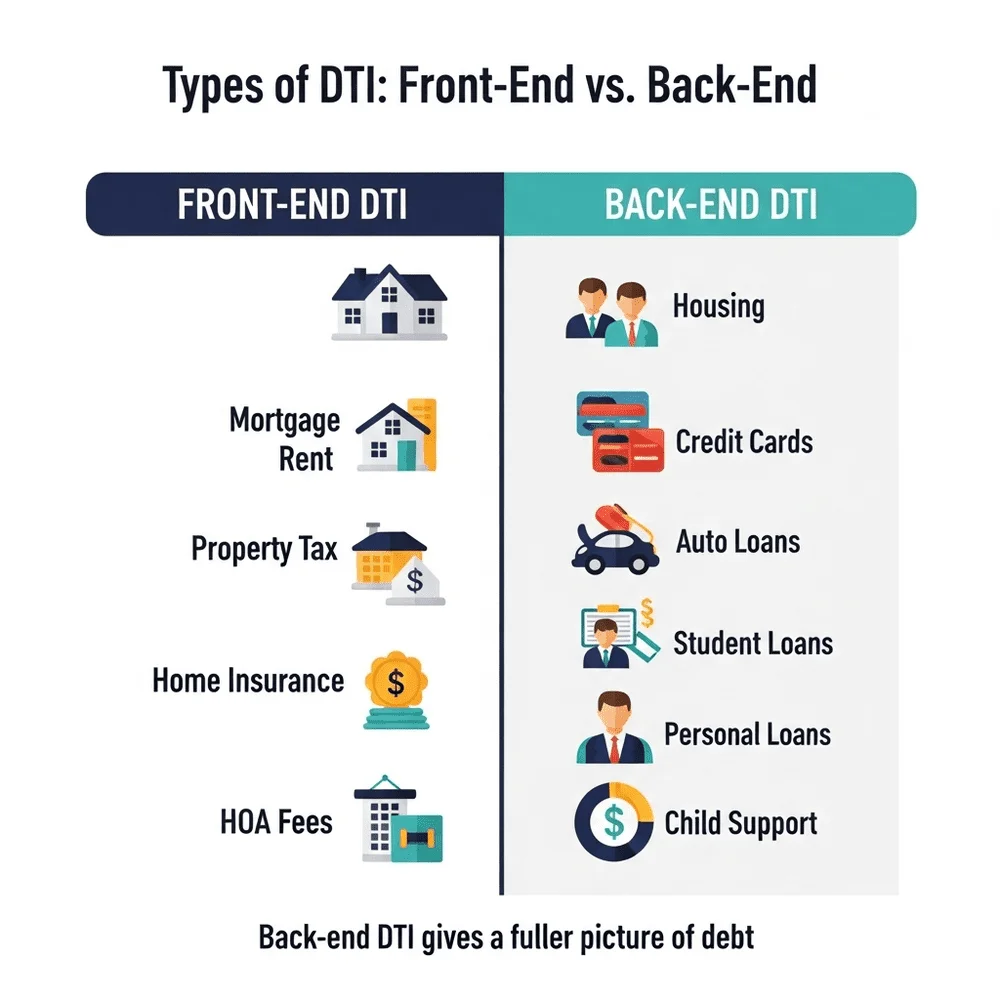

Types of DTI: Front-End vs. Back-End

Understanding both types can give you better clarity:

1. Front-End DTI

Includes only housing-related debts, such as:

- Mortgage or rent

- Property taxes

- Home insurance

- HOA fees

2. Back-End DTI

Includes all monthly debts, such as:

- Housing costs

- Credit card minimums

- Auto loans

- Student loans

- Personal loans

- Alimony/child support

Back-end DTI is generally preferred by most lenders because it offers a more comprehensive view of an individual’s total debt obligations.

What’s a Good DTI Ratio?

Here’s a general benchmark used by lenders:

- Under 20%: Excellent (Code 1)

- 21%–35%: Good (Code 2)

- 36%–45%: Fair (Code 3)

- Above 45%: Risky (Code 4)

Lenders typically look for a DTI ratio below 36%, especially when assessing eligibility for large financial commitments such as mortgages.

However, certain government-backed loan programs may accept higher DTI ratios if the borrower demonstrates strong compensating factors, such as a high credit score, consistent income, or substantial savings.

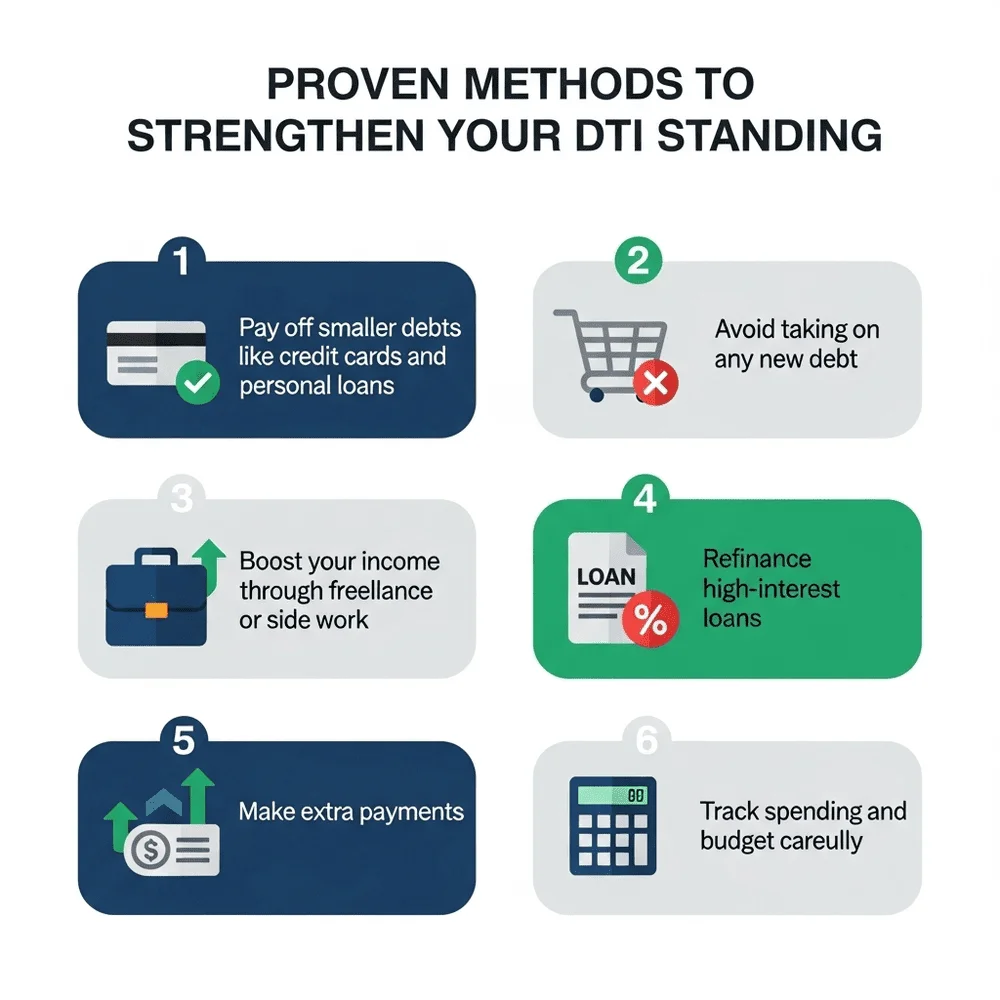

How to Improve Your DTI Code?

Even if your DTI code is on the higher side, there are actionable steps you can take to improve it. There are practical steps you can take:

- Pay off smaller debts first: Credit cards or personal loans

- Avoid new debt: Put a pause on big purchases

- Increase your income: Take freelance or side jobs

- Refinance high-interest loans: Lower your monthly payments

- Make Additional Payments: Even modest overpayments can gradually lower your principal balance and improve your DTI ratio.

- Track your expenses: A practical way to improve your DTI is to closely track your expenses and follow a disciplined budgeting plan to free up more of your monthly income.

Improving your DTI code can lead to more favorable loan conditions and increased long-term financial flexibility.

DTI Code vs. Credit Score

People often confuse DTI with credit score, but they’re very different:

| Feature | DTI Code | Credit Score |

| What it measures | % of income going to debt | Creditworthiness/history |

| Visibility | Often internal to lenders | Visible to consumers |

| Impact area | Loan approval, size, and terms | Interest rates, credit eligibility |

| How to improve | Reduce debt or increase income | Pay on time, reduce utilization |

You can have a great credit score but a bad DTI code if you earn well but owe too much.

DTI and Mortgages

DTI is especially important when applying for home loans. Most mortgage lenders won’t approve loans if your DTI is above 43%, which is the legal limit for qualified mortgages in many countries.

Some government-backed loans, like FHA or VA loans, may allow higher DTI if you meet other criteria, like a strong credit score or a large down payment.

Common Myths About DTI Codes

Let’s clear up a few popular misconceptions:

- Myth: DTI code is the same for everyone

Fact: Codes vary across lenders and regions. - Myth: Only low-income people have bad DTI

Fact: Even high earners can have bad DTI if they borrow too much. - Myth: The DTI code is not part of your credit report and is only used internally by lenders to assess your debt capacity.

Fact: It’s internal to lenders, not visible on your credit report - Myth: It takes years to fix a high DTI code

Fact: Paying off one loan can make a big difference quickly.

Real-Life Example

Let’s say Ali earns PKR 200,000/month and pays:

- PKR 30,000: Car loan

- PKR 20,000: Credit card

- PKR 50,000: Home loan

Total debts = PKR 100,000

DTI = (100,000 ÷ 200,000) × 100 = 50%

This puts him in DTI Code 4, which means a high-risk borrower. Ali should aim to pay off his credit card or refinance his home loan to reduce his debt and qualify for better terms in the future.

Final Thoughts

Understanding your DTI code helps you take charge of your financial future. A low DTI code leads to better loan offers, lower interest rates, and faster approvals. If your DTI is high, don’t worry, it can be improved through smart budgeting, reducing debt, and managing income wisely. While it doesn’t define you, your DTI code plays a key role in shaping your financial opportunities.